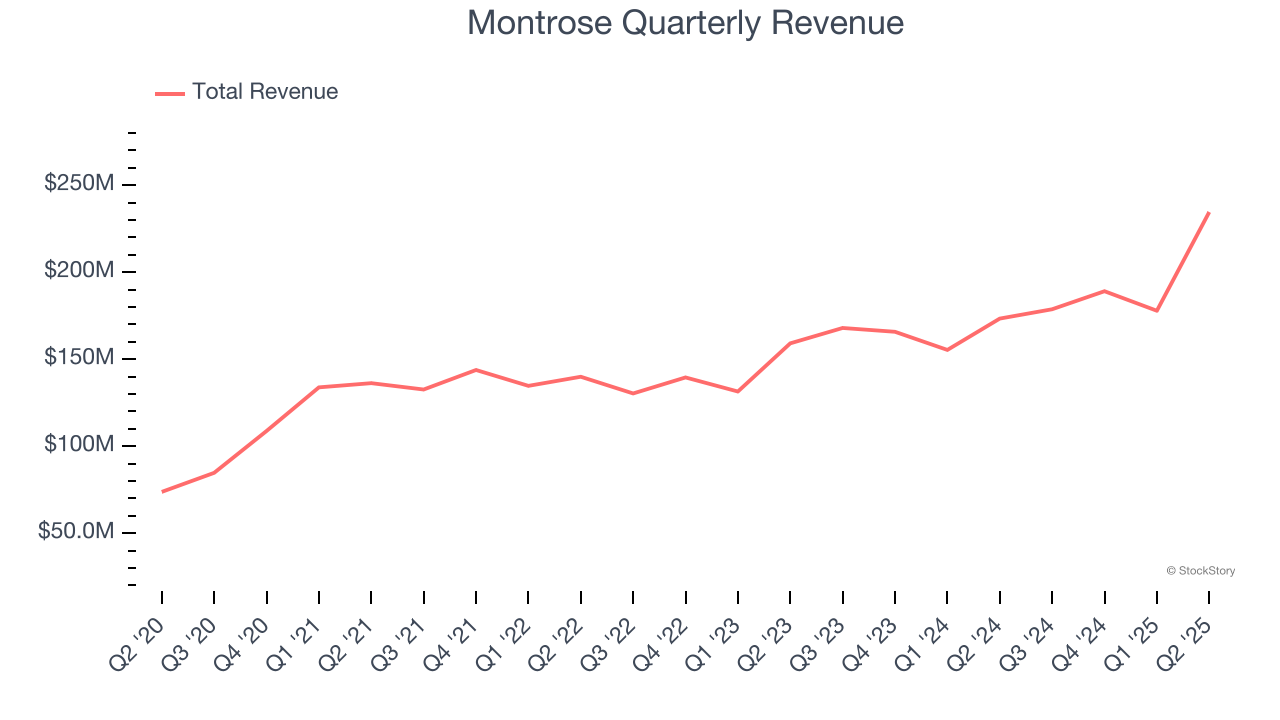

Environmental services provider Montrose (NYSE:MEG) reported Q2 CY2025 results exceeding the market’s revenue expectations, with sales up 35.3% year on year to $234.5 million. The company’s full-year revenue guidance of $815 million at the midpoint came in 7% above analysts’ estimates. Its non-GAAP profit of $0.63 per share was significantly above analysts’ consensus estimates.

Is now the time to buy Montrose? Find out by accessing our full research report, it’s free.

Montrose (MEG) Q2 CY2025 Highlights:

- Revenue: $234.5 million vs analyst estimates of $188.5 million (35.3% year-on-year growth, 24.4% beat)

- Adjusted EPS: $0.63 vs analyst estimates of $0.24 (significant beat)

- Adjusted EBITDA: $39.59 million vs analyst estimates of $27.33 million (16.9% margin, 44.8% beat)

- The company lifted its revenue guidance for the full year to $815 million at the midpoint from $760 million, a 7.2% increase

- EBITDA guidance for the full year is $114 million at the midpoint, above analyst estimates of $107 million

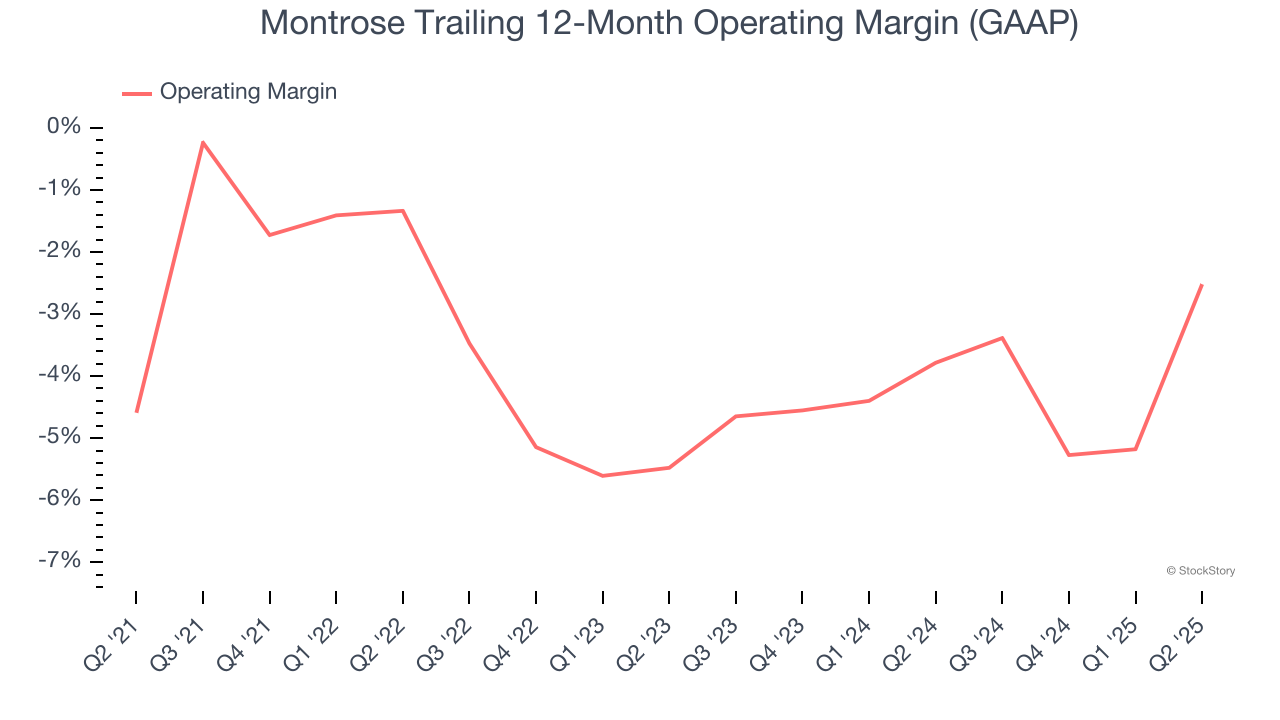

- Operating Margin: 6.4%, up from -1.5% in the same quarter last year

- Free Cash Flow was $19.93 million, up from -$9.76 million in the same quarter last year

- Market Capitalization: $773.6 million

Company Overview

Founded to protect a tree-lined two-lane road, Montrose (NYSE:MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

Revenue Growth

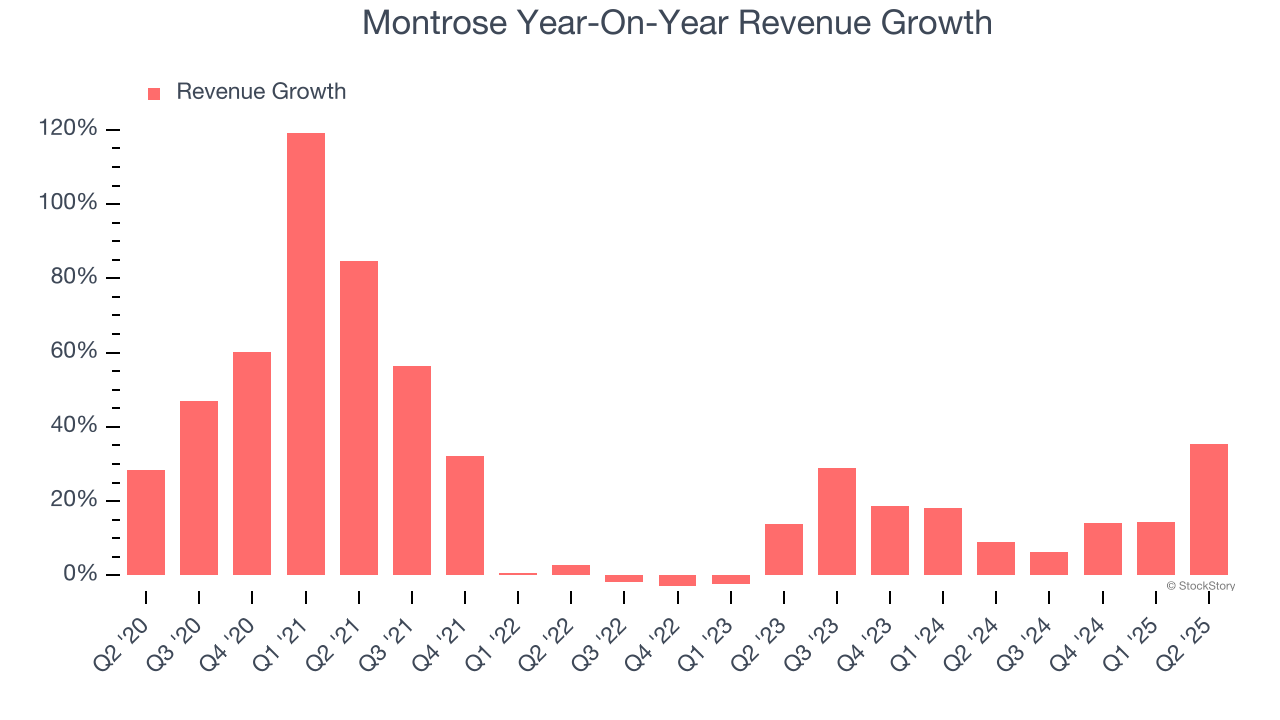

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Montrose grew its sales at an incredible 24.5% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Montrose’s annualized revenue growth of 18% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Montrose reported wonderful year-on-year revenue growth of 35.3%, and its $234.5 million of revenue exceeded Wall Street’s estimates by 24.4%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

Although Montrose was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 3.4% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Montrose’s operating margin rose by 2.1 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to show consistent profitability.

This quarter, Montrose generated an operating margin profit margin of 6.4%, up 7.9 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

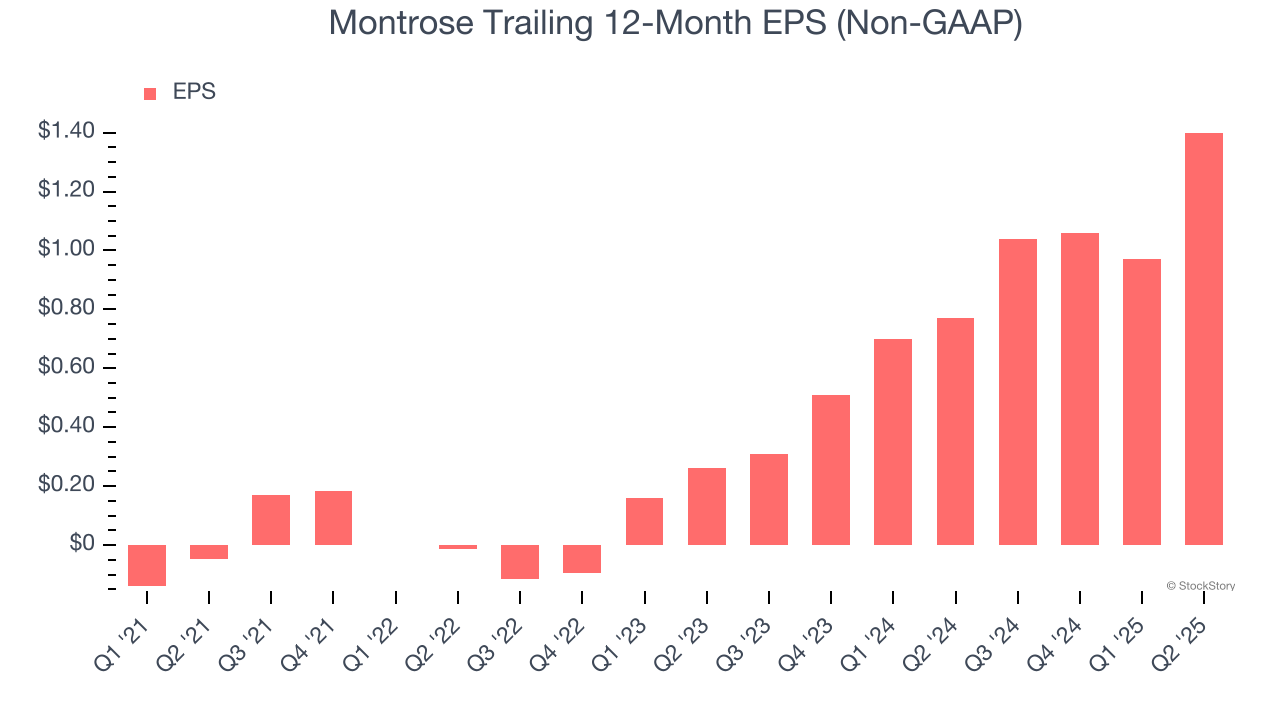

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Montrose’s full-year EPS flipped from negative to positive over the last four years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Montrose’s EPS grew at an astounding 132% compounded annual growth rate over the last two years, higher than its 18% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

We can take a deeper look into Montrose’s earnings to better understand the drivers of its performance. Montrose’s operating margin has expanded by 10.2 percentage points over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q2, Montrose reported adjusted EPS at $0.63, up from $0.20 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. We also like to analyze expected EPS growth based on Wall Street analysts’ consensus projections, but there is insufficient data.

Key Takeaways from Montrose’s Q2 Results

This was a beat and raise quarter. We were impressed by how significantly Montrose blew past analysts’ revenue, EBITDA, and EPS expectations this quarter. We were also excited its full-year revenue guidance was raised, a key sign that business momentum is improving. Zooming out, we think this quarter featured some important positives. The stock traded up 24.7% to $28.20 immediately following the results.

Montrose put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.