Even during a down period for the markets, OPENLANE has gone against the grain, climbing to $19.36. Its shares have yielded a 16.4% return over the last six months, beating the S&P 500 by 18.1%. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in OPENLANE, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

We’re happy investors have made money, but we're cautious about OPENLANE. Here are three reasons why you should be careful with KAR and a stock we'd rather own.

Why Is OPENLANE Not Exciting?

Facilitating the sale of approximately 1.3 million used vehicles in 2023, OPENLANE (NYSE:KAR) operates digital marketplaces that connect sellers and buyers of used vehicles across North America and Europe, facilitating wholesale transactions.

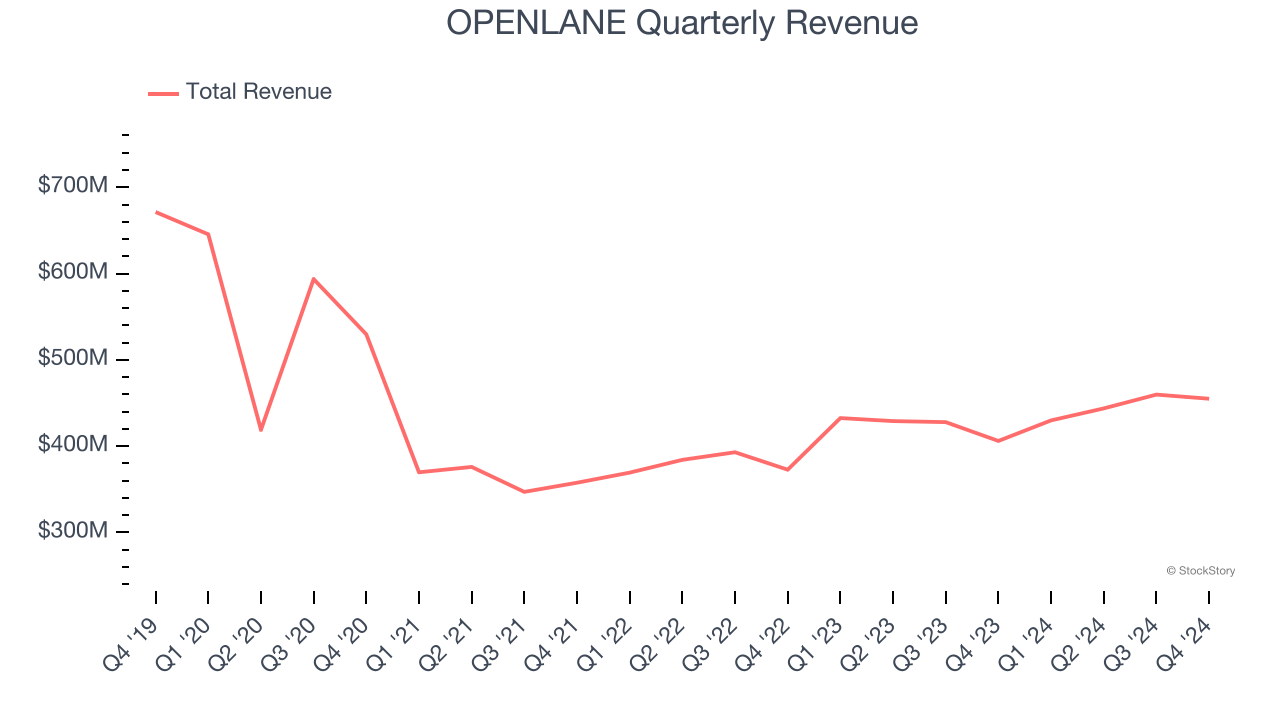

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, OPENLANE’s demand was weak and its revenue declined by 8.5% per year. This wasn’t a great result and signals it’s a lower quality business.

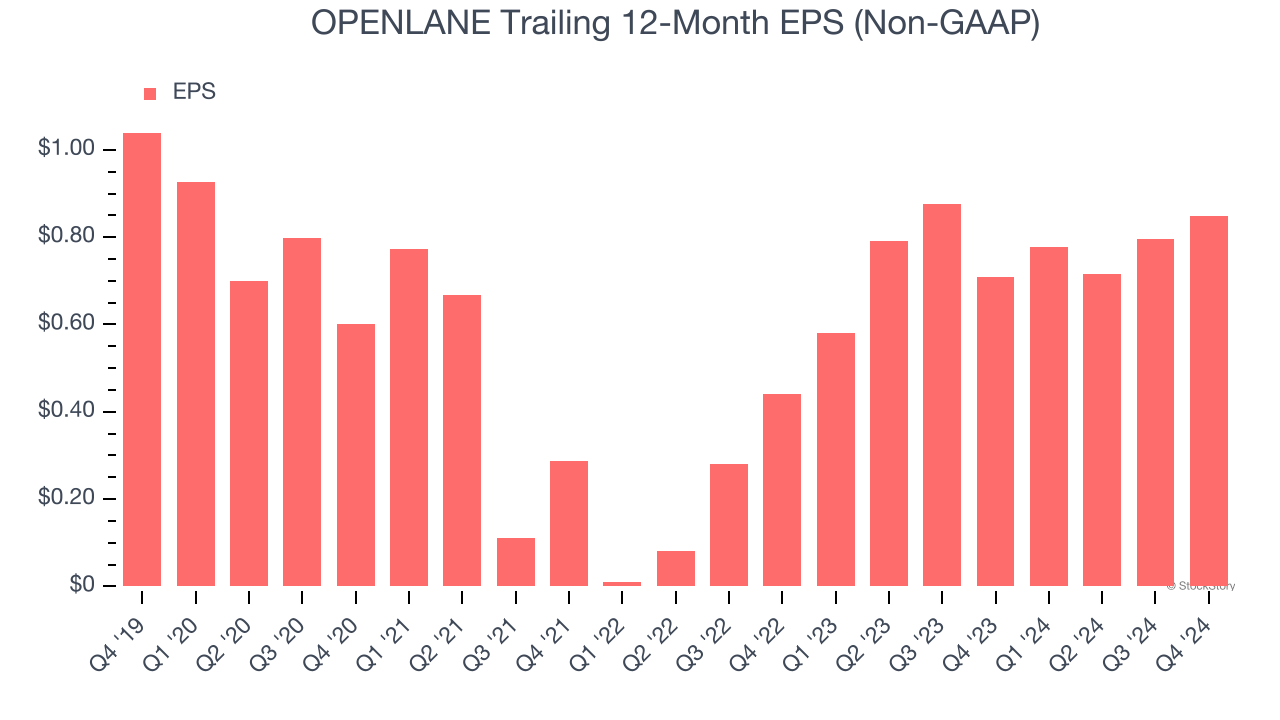

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for OPENLANE, its EPS and revenue declined by 4% and 8.5% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, OPENLANE’s low margin of safety could leave its stock price susceptible to large downswings.

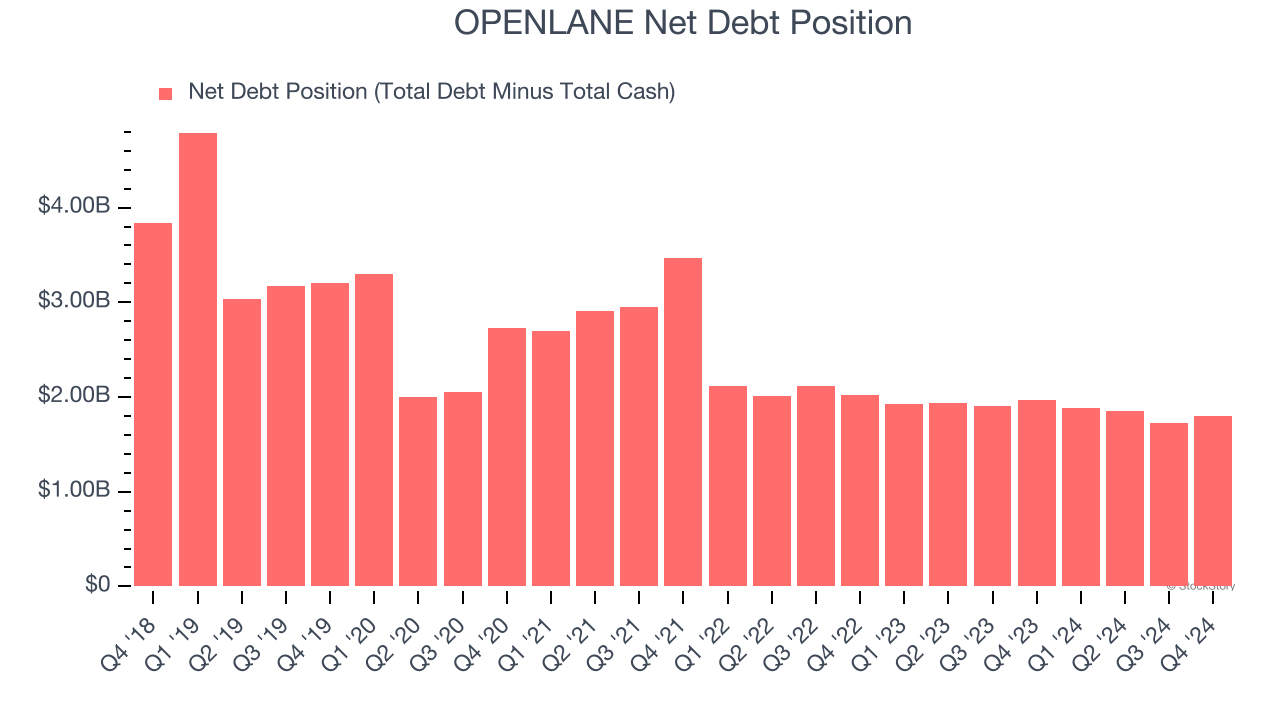

3. High Debt Levels Increase Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

OPENLANE’s $1.94 billion of debt exceeds the $143 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $293.4 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. OPENLANE could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope OPENLANE can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

Final Judgment

OPENLANE isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 19.8× forward price-to-earnings (or $19.36 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at one of our top digital advertising picks.

Stocks We Like More Than OPENLANE

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.